Most of you already know that your CIBIL score matters most when applying for a credit facility. Your CIBIL score can give you multiple benefits based if it's good (above 750) and vice-versa. This qualifying factor takes you to the next step of your loan approval process.

However, some borrowers with good credit profiles are rejected for their loan requests. Do you know why? It's better to understand the prime reasons behind such rejection cases with a short story.

What is a Credit Score?

A credit score is a three-digit number that defines your creditworthiness. Every borrower across the country has a credit score based on financial status. Multiple factors are considered to conclude a credit score. Different credit authorities consider different factors. TransUnion CIBIL is the popular authority to check the creditworthiness of any individual.

Now, let's move on to the story.

Rohit is a private employee drawing a handsome salary of 1 lakh per month. This salary is far enough to manage a good lifestyle. Recently Rohit planned to buy a car with a small upfront amount convert the rest into EMI.

Talking about his past financial journey, he owns one credit card and an ongoing home loan. Interestingly, he has never missed any bill/EMI payment on the credit card and home loan.

Unfortunately, when he applied for the car loan, he got an overdue amount mentioned in his credit report which resulted in his loan request rejection.

This looks weird when Rohit has never missed any payment. So, what actually resulted in this problem?

Well, the entire story revolves around the CIBIL report that banks/lenders receive from the Credit authority. The most possible and practical reason for this situation is an unattended error in the CIBIL report that resulted in his loan rejection.

Most of you must be aware of the common CIBIL errors you can see in your CIBIL report.

Low Credit Score: Ultimately, this is the number that you manage your finances and pay the bills on time. Regardless of the unseen reasons, you might see a bad credit score on your credit report, even when you have no overdue backlogs.

Mistakes in Your Personal/Account Details: It looks type, but a small typo in your personal details or account details can lead to big troubles, rejection for your loan request being one of them. The typo can be major or minor; interestingly, both are problematic for your financial journey.

Days Past Due (DPD): Do you know that Credit Authorities create your CIBIL score based on the details & data they receive from different lenders and banks? Under RBI regulation, all lenders/banks need to share the borrower's latest details with the CIBIL authorities in India.

However, if the CIBIL authority doesn't receive your bill payment details, they are considered missed payments and marked under Days Past Due.

For all the pending amounts in your credit report, your DPD will be indicated with "XXX" Remember, "000" means you don't have any pending bills to pay.

Errors in Your Loan Account: If you have taken loans in the past and paid them on time, that information may not be available to the CIBIL authorities. This results in half knowledge; hence, the same is displayed on your credit report.

Any half-information about your closed account may be tagged as 'written off' or 'settled', in your report, which signals a bad credit score.

Wrong Overdue Information: Your credit score might have overdue account information, even when the account is timely paid off with no overdue pending.

Duplicate Loan Accounts: You might also see more than one loan account with the same account details. This creates big trouble if you have missed any payment on one account; the same will be added to its counterfeit.

Understanding the root cause of Rohit's loan request rejection is one aspect. But, the major part is how you can correct these details and file a dispute for the errors.

Before filing a dispute, you must know the difference between minor and major errors.

Minor Errors: It includes misspelled names, incorrect date of birth, addresses, etc. You must note that minor errors have no impact on your credit score. Moreover, they are often easy to resolve.

Major Errors: These mistakes can significantly lower your CIBIL report. Examples include linking the wrong credit account to your report, having an amount already closed but marked as"settled" in your report, etc.

So, what is the step-by-step process to file a CIBIL error dispute?

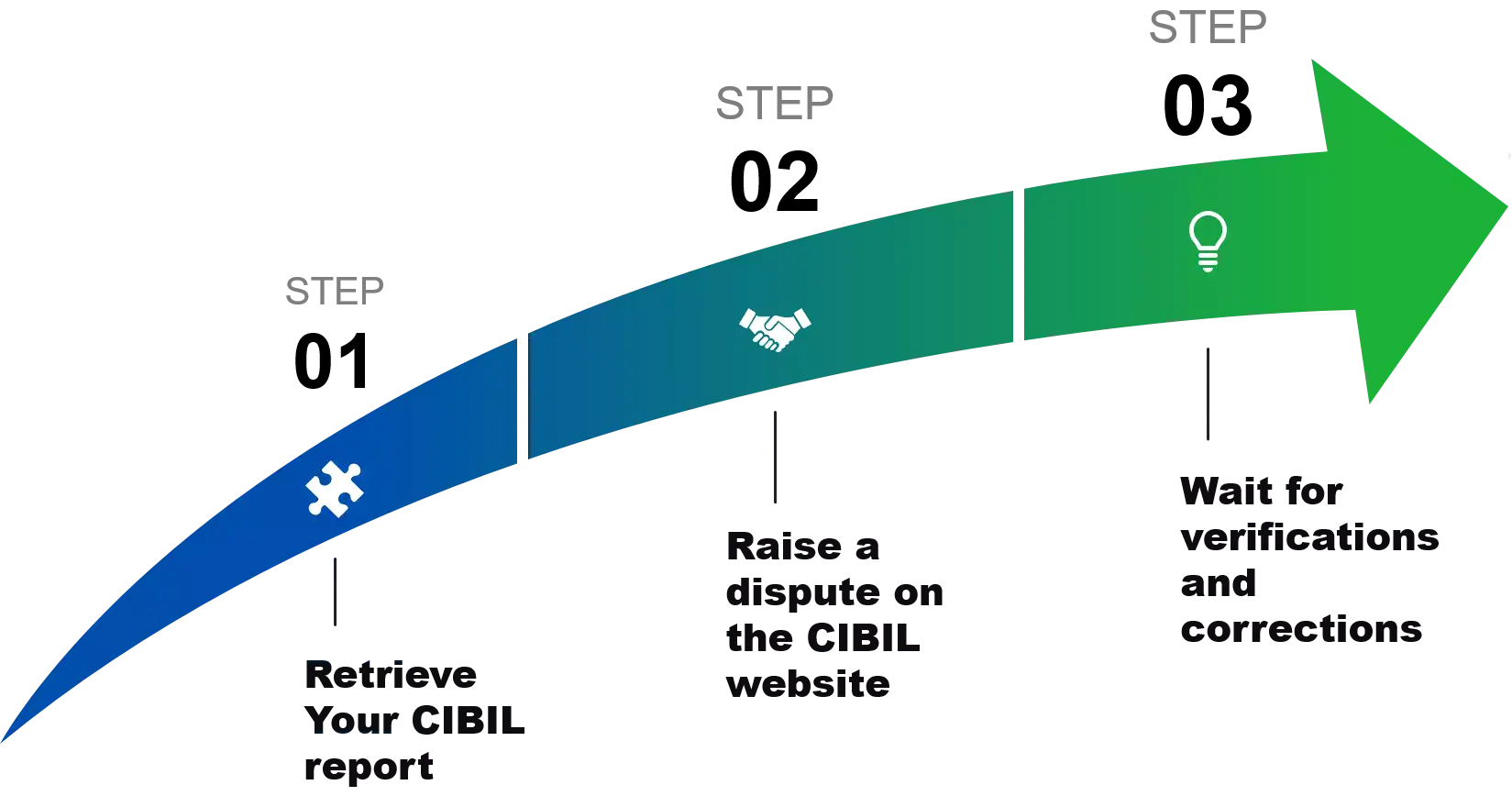

Below are the three-step processes that you can follow to file your dispute.

Step 1: Retrieve Your CIBIL Report: There are four credit bureaus in India. CIBIL is the most used credit bureau that most banks/lenders consider to check your loan eligibility. The First step includes downloading your credit report from the official website. In the downloaded report, enlist all the issues.

Step 2: Raise the Dispute on CIBIL Official Website: Now you have the list of issues (if more than one). It's time to visit the official website of CIBIL and file your dispute for correction. Follow the steps given below to complete the dispute filing process.

Step 3: Wait for the Verification & Corrections: Once everything is done from your end, the ball is now in the hands of CIBIL authority. They will forward your request to the concerned bank to get a clarification. Based on their clarification, your CIBIL report will be updated with the correct details. It's important to note that the CIBIL authority will update your records based on what they receive from the respective banks. Moreover, you need to wait for at least 30 days to get an update from the CIBIL authority.

Which fields in a Credit report can you file a dispute?

Every borrower needs to know the fields you can correct via the CIBIL dispute process. Below are the fields in which you can file the dispute.

Among the list mentioned above, minor errors are easy to resolve, while the major ones take time (atleast 30 days) for correction.

If anyone (like Rohit) has faced this scenario, they must immediately diagnose the credit report for any error. Often lenders/banks give you the reason for rejection that you should take as the sign of any CIBIL report error.

Once your issues and errors are resolved in the credit report, you can reapply for the new credit loan and get it approved quickly.

What if CIBIL doesn't respond to your dispute query?

You may get unsatisfied or no result from the CIBIL authority after 30 days. If one of the candidates gets unsatisfactory results from the authority, you should follow the process from scratch. Yet, if nothing works, you can reach the Bank ombudsman to raise the dispute to a higher authority.

Check Your CIBIL Report Regularly

Financial experts always recommend reviewing your credit report regularly. Remember, checking your credit report won't impact your credit score. However, with frequent checks made by the bank/lender, your CIBIL score is affected as you are marked as a "credit-hungry" borrower.

Checking your CIBIL report is beneficial for multiple reasons; below are some of them.

Save You From Last Minute Efforts: With timely checks, you can get an update about any CIBIL report error that you can file immediately. Skipping it may lead to late loan disbursal or rejection until credit report errors are rectified.

Save You From Credit Frauds: Nowadays, identity theft is common under which your details are used to get credit facility (perosnal loan, payday loan, etc.) and is left unpaid. You should take immediate action as soon as you know about the identity theft.

Tell You About the Current Credit Score: It's necessary to know your credit score before applying for any loan. Hence getting insight into your credit report to know the score.

If your score exceeds 750, you can stay assured of getting a good offer on your credit facility.

Filing a CIBIL Dispute isn't tough.

Many of you have now understood how simple the process of filing your CIBIL error dispute is. Interestingly, there is also an offline process for the corrections. In the offline mode, you need to send a letter to the registered authority along with the error information and corrections proof.

You can send the letter to Credit Information Bureau (India) Ltd, Hoechst House, 6th Floor, 193, Backbay Reclamation, Nariman Point, Mumbai 400 021.

Need help in resolving your CIBIL dispute? Speak to a certified Credit Counsellor

Apply Now

1. Just fill up a simple form

2. Validate your details

3. Click on Submit button

1. Wide range of options

2. Customised loan solutions

3. Best deal on your loan

1. Priority processing by lender

2. Timely Feedback on your application